Britain’s energy crisis is no longer about fuel. It is no longer even about technology. It is about systems, incentives, and financial structures that have drifted so far from physical reality that they now require political management to survive. No company better illustrates this than Octopus Energy. The poster child of the UK’s Net Zero transition, the darling of ministers, and now, quietly, a warning sign.

On paper, Octopus looks like a triumph. It has millions of customers. It owns stakes in flagship renewable assets. It runs Kraken, the much-hyped energy software platform that is supposedly the envy of the world. It talks the language of innovation, disruption and green progress fluently. But underneath the marketing, a far more troubling picture is emerging.

A company exposed to the most grid-constrained parts of Britain, operating in a system that cannot use the power it is building, and now financially re-engineering itself under regulatory pressure , with the state stepping quietly inside the structure.¹²

Start with the physical reality. Octopus’s renewable portfolio is heavily concentrated in exactly the parts of the country where the grid is already broken.

It holds a significant stake in East Anglia One, one of the largest offshore wind farms in Britain.³ It is also exposed to the Yorkshire and North Sea corridors through projects like Hornsea and Walney.⁴ These are not random locations. They are the most congested export routes in the country , the places where wind is already being paid to switch off because the grid cannot move the power south.⁵

East Anglia is the clearest example of the national delusion. Politicians boast about the scale of offshore wind being built there, yet the onshore transmission reinforcements needed to move that power into the rest of the system are years late, mired in planning disputes, transformer shortages, and public opposition.

National Grid’s own “Beyond 2030” and East Coast reinforcement plans show that full reinforcement of this corridor will not be complete until well into the 2030s.⁶⁷ In other words, we are building generation that the country cannot use.

This is not a temporary glitch. It is structural. The UK has chosen to approve generation first and hope the grid catches up later. It isn’t. The result is a system where turbines spin, power is curtailed, and consumers pay twice:

once for the wind farm, and again for the gas plant that has to run elsewhere to keep the lights on. Constraint payments have already reached

In this world, renewable assets increasingly cease to be energy assets in the normal sense. They become regulatory assets , their revenues shaped less by delivering useful power than by contracts, constraint payments, and political rules. They may still look fine in a fund prospectus. They may still produce acceptable financial returns. But systemically, they are not solving the problem they are supposed to exist to solve.⁹

Now look at Octopus’s corporate structure. The real financial stress signal in the group is not coming from the generation side. It is coming from the retail supply business. Under Ofgem’s post-crisis rules, suppliers are now required to hold large amounts of real, tangible capital relative to their customer base.¹⁰ Octopus’s extraordinary growth has turned this into a problem. The bigger it gets, the more capital it is supposed to hold. And it does not have enough.¹¹

The accounts show a company that has swung from profit into large losses, whose cash flow has been propped up by working-capital timing, and which has required repeated shareholder injections just to stand still.¹² This is not the profile of a boring, stable utility. It is the profile of a growth business that has hit the wall of regulation and arithmetic.

And this is where Kraken enters the story.

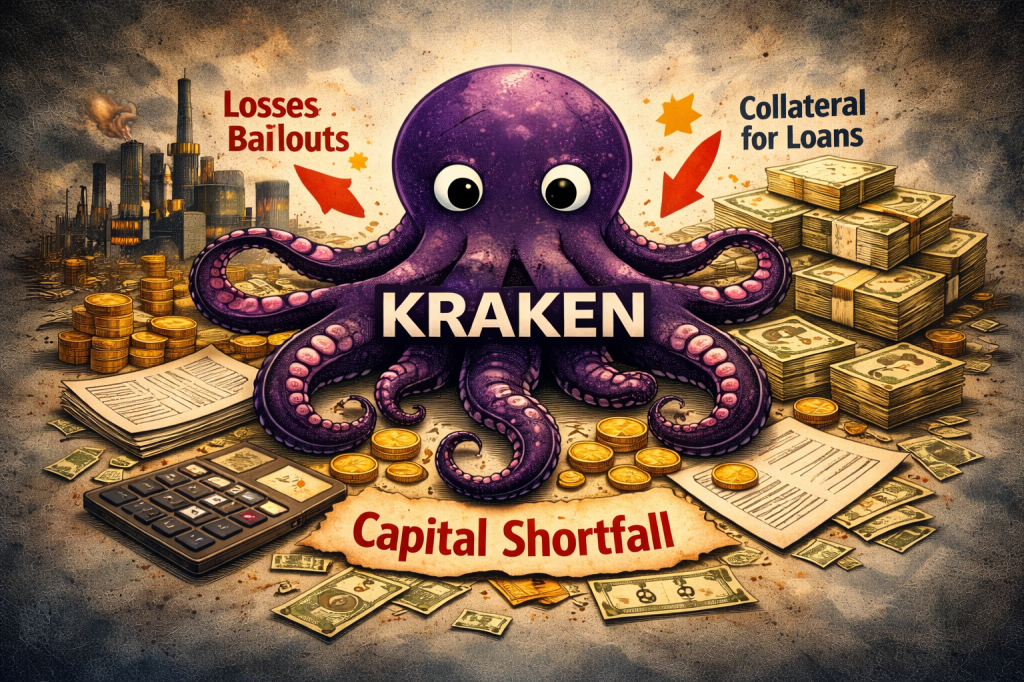

Kraken is presented as a triumph: a world-class software platform, serving tens of millions of accounts, valued at billions.¹³ But in the small print of the group’s financial structure, Kraken is doing something much more prosaic. It is being used as collateral. It is guaranteeing the group’s liquidity facilities. The crown jewel is being pledged to support the rest of the business. That is not how healthy corporate structures work. That is what happens when lenders want security and the balance sheet is under strain.¹²

The decision to spin out and sell stakes in Kraken is therefore not really about “scaling a tech platform”. It is about capital. It is about converting an illiquid internal asset into cash and regulatory comfort. It is about plugging a structural hole.¹²

And then comes the most politically sensitive part of all: the state.

The UK government has now taken a stake in Kraken.¹⁴ Officially, this is about backing British tech. In reality, it places the state directly inside the only asset that is stabilising one of the country’s largest energy suppliers at a moment of regulatory and financial pressure. Even if nobody intends it, this is how “too big to fail” structures are born.

The moment the state has skin in the game, the moment millions of customers depend on the company, the moment a disorderly failure becomes unthinkable, the rules change.

At that point, risk is no longer allowed to crystallise. It is managed. Deferred. Socialised.

This is the deeper pattern of the entire Net Zero energy transition.

We are not building an engineering system. We are building a financial and political system that tries to compensate for the absence of one. We build generation where the grid cannot carry it. We stabilise the consequences with subsidies, constraint payments, and regulatory instruments. We allow companies to grow into systemic importance. And then we discover they cannot be allowed to fail.¹⁵

Octopus is not a villain in this story. It is a case study.

It shows what happens when targets replace system design. When finance replaces engineering. When politics replaces physics.

Britain does not have an energy shortage. It has a grid shortage. It does not have a technology problem. It has a system architecture problem. And until that is faced honestly, we will keep building impressive-looking assets that do not fix the problem, and impressive-looking companies that quietly become too important to be allowed to fall over.¹⁶

The danger is not that Octopus collapses tomorrow. The danger is that, piece by piece, Britain is recreating a fully politicised, financially engineered energy system in which failure is impossible, costs are opaque, and reality is always postponed to the next upgrade, the next reform, the next spending round.

That is not an energy transition.

It is a slow-motion institutional trap.

Sources & Footnotes

1. Ofgem, Financial Resilience and Capital Adequacy for Suppliers, 2023–2024 reforms.

2. Kathryn Porter, Watt-Logic, Octopus and Kraken are swimming in murky waters, 27 Jan 2026.

3. Octopus Energy Generation / Vector Renewables press release: 10% stake in East Anglia One.

4. Octopus/GLIL/Hornsea and Walney offshore wind fund disclosures.

4. NESO / National Grid ESO constraint and curtailment statistics 2023–2025.

5. National Grid, Beyond 2030: East Coast & East Anglia Reinforcement Plans.

6. NESO, Holistic Network Design & East Coast Cluster documents.

7. NESO Constraint Costs reports; £2–3bn+ annualised constraint costs.

8. UK NAO & Public Accounts Committee reports on curtailment and system inefficiency.

9. Ofgem Capital Adequacy rules post-supplier-collapse crisis.

10. Financial Times & Ofgem commentary on Octopus capital requirements.

11. Octopus Energy Group filings;

12. Watt-Logic forensic analysis.

13. Octopus / Kraken valuation and US investment round announcements (2024–2025).

14. UK Government announcement of stake in Kraken (DSIT / British Business Bank).

15. NAO, CCC, and Parliamentary reports on Net Zero delivery risks and systemic cost.

16. NESO, Clean Power 2030, and grid delivery timelines showing 2030s bottlenecks.

Leave a comment