The United Kingdom is entering a period of acute strategic vulnerability. Over the past decade, the assumptions that shaped much of Western policy have begun to collapse. The era of easy globalisation, cheap imported goods, frictionless logistics, stable geopolitics, and rules-based optimism has given way to a more insecure world defined by rivalry, supply risk, industrial competition, and the return of hard national interest. Britain, however, has been slow to recognise the scale of this change. Instead of reorienting itself toward resilience, sovereignty, and productive strength, it has continued to pursue a model that depends on openness, external stability, and policy frameworks that increasingly sit uneasily with geopolitical reality.[1]

This is not merely a question of rhetoric. It is visible in the structure of the British economy itself. Manufacturing employment in the United Kingdom fell from 4.284 million in 1997 to 2.715 million in 2018, according to the Office for National Statistics, reflecting a long-term hollowing out of domestic productive capacity.[2] That decline was not simply the result of technological change. It was also the outcome of a political economy that favoured financialisation, global sourcing, and service-sector expansion over industrial resilience. For years, this was presented as modernisation. In truth, it left Britain more exposed to external shocks and less able to meet strategic needs from within.

The fragility of that model became impossible to ignore after the pandemic and the energy shock that followed Russia’s invasion of Ukraine. Supply chains failed, transport routes clogged, input costs surged, and the dependence of European economies on external energy and manufacturing systems was laid bare. In Britain, these pressures were magnified by an economy already marked by weak domestic production, high energy costs, and an electricity market unusually sensitive to gas prices. The Office for National Statistics has noted that in 2021 gas-fired generation accounted for 43 per cent of UK electricity generation but set the market price 97 per cent of the time, helping explain why UK industrial electricity prices became so elevated relative to peers.[3]

By 2023, the UK had the highest industrial electricity prices in the IEA comparison set, with prices 46 per cent above the IEA median and almost 50 per cent higher than France and Germany, while standing around four times those in the United States and Canada.[4] This is one of the clearest measurable signs that Britain’s present economic model is under strain. A country that wishes to remain a serious industrial economy cannot indefinitely sustain power prices so far above those of its main competitors. That is not merely an energy issue. It is a question of national capability.

At the same time, the world’s major powers have been moving in a different direction. The United States, China, and Russia have not all followed the same path, nor do they share the same political systems or strategic aims. Yet all three have shown a willingness to place national interest, industrial capacity, and energy security ahead of rigid ideological consistency. This is the real dividing line. The question is no longer whether states speak the language of climate diplomacy, multilateralism, or global cooperation. The question is what they actually do when growth, power, security, and sovereignty are at stake.

The United States offers the clearest example of this reordering of priorities. On 20 January 2025, the White House ordered the withdrawal of the United States from the Paris Agreement, and the UN treaty record states that the withdrawal took effect on 27 January 2026.[5] Yet even before that formal departure, American policy had already been moving toward a more openly strategic form of industrial nationalism. The Inflation Reduction Act channelled $369 billion into energy and climate-related incentives, while the CHIPS and Science Act drove tens of billions of dollars of semiconductor investment with an explicit goal of rebuilding domestic production capacity and securing critical supply chains.[6] In other words, even when Washington talked about climate, it increasingly acted through the logic of industrial policy, state capacity, and national advantage.

China’s position is, if anything, even more revealing. Officially, Beijing remains committed to peaking carbon dioxide emissions before 2030 and achieving carbon neutrality before 2060.[7] Yet the same state that speaks the language of green transition continues to build coal-fired power at scale. Global Energy Monitor reports that China commissioned 30.5 GW of new coal capacity in 2024 and started construction on 94.5 GW more, the highest level of new construction starts in nearly a decade.[8] This is not a contradiction once one understands Beijing’s real hierarchy of priorities. China is willing to expand renewables aggressively, but it is not prepared to gamble industrial continuity, system stability, or geopolitical leverage on intermittency alone. Energy security remains paramount.

Russia, for its part, also illustrates the difference between formal participation and practical priority. Moscow remains within the Paris framework and in 2025 submitted a second nationally determined contribution setting a 2035 emissions target of 65–67 per cent of 1990 levels, taking account of forest absorptive capacity.[9] Yet Russia’s conduct since 2022 has made abundantly clear that climate policy is subordinate to resource power, strategic survival, sanctions management, and the use of energy exports as an instrument of statecraft. Russia has not organised itself around decarbonisation as a governing principle. It has organised itself around national endurance under pressure.

This is where Britain’s problem becomes stark. The major powers may differ in ideology, but all of them have shown a willingness to adapt policy to material reality. Britain, by contrast, has too often treated targets, frameworks, and aspirations as though they were a substitute for capability. It has embraced climate ambition more rigidly than strategic realism, while failing to ensure the infrastructure, price structure, and industrial base needed to support the transition on competitive terms. That has left the country in an increasingly uncomfortable position: morally assertive, but structurally weak.

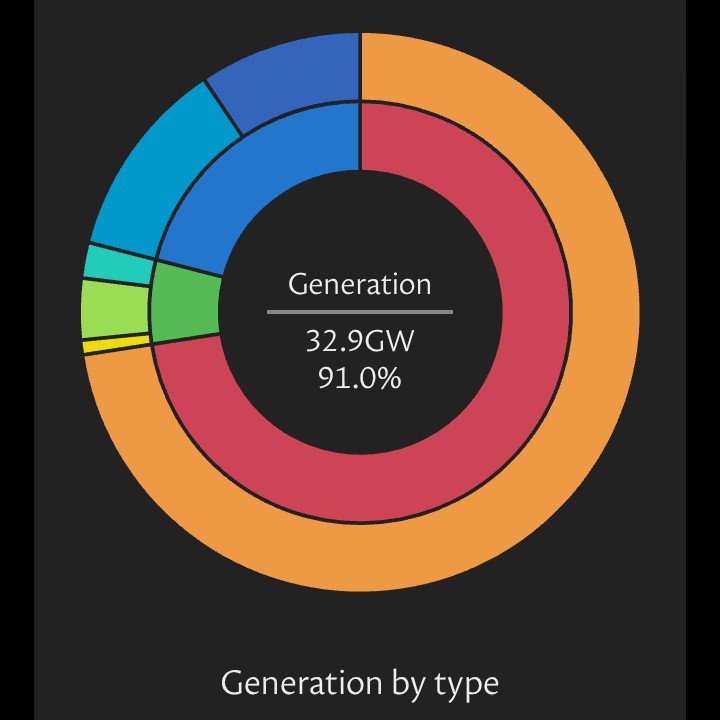

The grid itself is a case study in that weakness. NESO has stated that the old grid connections queue had grown to over 700 GW, around four times what Great Britain needs by 2030, and that the queue had become clogged with projects that were not ready or not aligned to actual deliverability.[10] In December 2025, NESO said that more than 300 GW of projects in the old queue would not move forward at that stage under the reformed pipeline.[11] This is not a minor technical problem. It is evidence of a system that has spent years licensing ambition without matching it to transmission readiness, engineering sequence, or real-world buildability. Britain has accumulated the appearance of progress while embedding delay and confusion into the heart of its energy system.

The consequence is not only delay but cost. Parliamentary answers drawing on NESO balancing data show that in 2024/25 wind generators were paid about £370 million to turn down output, while the cost of turning up gas generation to replace curtailed supply was £910 million.[12] Earlier answers recorded total constraint costs of £1.4 billion in 2023.[13] The point is not that renewables are uniquely to blame. The point is that Britain has developed a system in which generation, transmission, and market design are increasingly misaligned, and the public pays for the mismatch. An energy strategy that repeatedly produces electricity in one place, cannot transport it efficiently, and then pays to suppress it while calling on alternative generation elsewhere is not a mark of a mature system. It is a sign of distortion.

Meanwhile, the rhetoric of parts of the global financial and technological elite has also begun to shift. BlackRock, the world’s largest asset manager, left the Net Zero Asset Managers initiative in January 2025. Reuters reported that the move came amid political and legal pressure in the United States, and that the wider initiative suspended activities shortly afterwards.[14] At the same time, BlackRock’s own 2026 outlook places artificial intelligence at the centre of its macro and investment framework, while its market commentary highlights the growing link between energy security and AI-driven demand.[15] This does not mean climate has disappeared. It means the emphasis is changing. The decisive issue is no longer symbolic alignment alone, but who can build and power the infrastructure of the next economic era.

Bill Gates represents a subtler version of the same shift. He has not abandoned climate concerns, nor has he ceased promoting low-carbon innovation. But his recent writing places greater emphasis on cheap clean energy, energy innovation, adaptation, and human welfare than on abstract temperature metrics alone.[16] In one essay he argues explicitly for a climate strategy focused “even more than temperatures or greenhouse gas emissions” on human welfare.[17] That is not a repudiation of climate policy. It is, however, a recognition that the world cannot be governed on slogans. Energy abundance, technological realism, and social outcomes matter.

Artificial intelligence is accelerating this wider realignment. The IEA projects that global electricity consumption by data centres will more than double to around 945 TWh by 2030, with AI the single most important driver of that growth.[18] BlackRock’s 2026 outlook likewise frames AI as a macro force shaping revenue, investment, and infrastructure allocation across the economy.[19] Put bluntly, the next phase of technological competition will be power-hungry. It will reward systems that can supply reliable electricity at scale, process planning applications quickly, build transmission fast, and sustain industrial capex over many years. Countries that cannot do these things will not lead the next era. They will rent it from those that can.

That is why the United Kingdom’s current trajectory is so concerning. Britain remains burdened by high industrial electricity prices, a grid backlog measured in hundreds of gigawatts, and an economic model that has shed much of its manufacturing strength while aspiring to lead in areas that demand ever more power, infrastructure, and strategic coordination.[20] It is trying to live simultaneously in two worlds: one built on post-Cold War assumptions of benign interdependence, and another increasingly defined by continental-scale competition, energy realism, and industrial statecraft. The tension between those two worlds is now becoming economically and politically unsustainable.

None of this requires a rejection of international cooperation, nor does it require abandoning environmental stewardship. It does, however, require a far more honest assessment of what the world has become. The major powers are not organising themselves around self-imposed weakness. They are pursuing climate goals, where they pursue them at all, through the lens of sovereignty, security, and competitive advantage. Britain has too often done the reverse. It has behaved as though declarations, targets, and institutional virtue could compensate for industrial decline, infrastructure lag, and strategic dependency. They cannot.

The lesson is therefore plain. In a harder world, resilience is not a slogan. It is the precondition of freedom. A state that cannot generate affordable power, defend its industrial base, shorten critical supply chains, and build vital infrastructure in the right order will find that many of its choices are no longer truly its own. The United Kingdom is in trouble not because the world changed, but because others adapted more quickly to that change. Britain still has the means to correct course. What it no longer has is the luxury of pretending that the old model remains sufficient.

Footnotes and References

[1] Office for National Statistics, Long-term trends in UK employment: 1861 to 2018, 29 April 2019; Office for National Statistics, The impact of higher energy costs on UK businesses: 2021 to 2024, 19 May 2025; House of Commons Library, Gas and electricity prices during the “energy crisis” and beyond, 25 February 2026. �

Office for National Statistics +2

[2] Office for National Statistics, UK Workforce Jobs SA: C Manufacturing (thousands), series JWR7, accessed 11 April 2026. The series records 4.284 million manufacturing workforce jobs in 1997 and 2.715 million in 2018. �

Office for National Statistics

[3] Office for National Statistics, The impact of higher energy costs on UK businesses: 2021 to 2024, citing research on gas as the marginal price setter in UK electricity markets. �

Office for National Statistics

[4] Office for National Statistics, The impact of higher energy costs on UK businesses: 2021 to 2024; Department for Energy Security and Net Zero, International non-domestic energy prices, updated 27 November 2025. �

Office for National Statistics +1

[5] The White House, Putting America First In International Environmental Agreements, 20 January 2025; United Nations Treaty Collection, Paris Agreement status entry for the United States, noting notice of withdrawal on 27 January 2025 and effect from 27 January 2026. �

The White House +1

[6] U.S. Department of the Treasury, Treasury Announces Guidance on Inflation Reduction Act’s Strong Labor Provisions, 29 November 2022; U.S. Department of Commerce, Two Years Later: Funding from CHIPS and Science Act Creating Quality Jobs, Growing Local Economies, and Strengthening America’s National Security, 9 August 2024. �

U.S. Department of the Treasury +1

[7] UNFCCC, China’s Achievements, New Goals and New Measures for Nationally Determined Contributions, stating that China will peak CO2 emissions before 2030 and achieve carbon neutrality before 2060. �

UNFCCC

[8] Global Energy Monitor et al., Boom and Bust Coal 2025, reporting that China commissioned 30.5 GW of coal capacity in 2024 and began 94.5 GW of new coal construction. �

Global Energy Monitor +1

[9] UNFCCC, Russian Federation Second NDC, submitted September 2025, setting a 2035 target of 65–67 per cent of 1990 emissions levels, taking into account absorptive capacity. �

UNFCCC +1

[10] NESO, Connections Reform Results, stating the queue had grown to over 700 GW, around four times what is needed by 2030. �

National Energy System Operator (NESO)

[11] NESO, NESO implements electricity grid connection reforms to unlock investment across Great Britain, 8 December 2025, stating that more than 300 GW of projects in the old queue would not move forward at that stage. �

National Energy System Operator (NESO)

[12] UK Parliament written answer on wind curtailment and balancing costs, citing NESO’s 2025 balancing cost report: £370 million paid to wind generators to turn down in 2024/25 and £910 million for gas turn-up. �

UK Parliament Questions

[13] UK Parliament written answer, 25 April 2024, stating that total constraint costs in 2023 were £1.4 billion. �

UK Parliament Questions

[14] Reuters, BlackRock quits climate group as Wall Street lowers environmental profile, 9 January 2025; Reuters, Investor climate group suspends activities after BlackRock exit, 13 January 2025. �

Reuters +1

[15] BlackRock Investment Institute, 2026 Investment Outlook; BlackRock weekly market commentary, 29 March 2026, noting that energy security and AI-driven demand are reinforcing one another. �

BlackRock +1

[16] Bill Gates, The Year Ahead 2026: Optimism with Footnotes; Gates Notes energy innovation page. �

gatesnotes.com +1

[17] Bill Gates, A new approach for the world’s climate strategy, arguing for a strategy focused more on human welfare than on temperature or emissions metrics alone. �

gatesnotes.com

[18] International Energy Agency, Energy and AI, projecting that global data-centre electricity consumption will more than double to around 945 TWh by 2030. �

IEA +1

[19] BlackRock Investment Institute, 2026 Global Outlook and related 2026 outlook materials highlighting AI as a macro force with major implications for infrastructure, productivity, and capital allocation. �

BlackRock +2

[20] Office for National Statistics, UK Workforce Jobs SA: C Manufacturing (thousands); Office for National Statistics, The impact of higher energy costs on UK businesses; NESO, Connections Reform Results. �

Office for National Statistics +2

Leave a comment