There was a time when Octopus Energy presented itself as the disruptor of Britain’s broken energy market , a fresh, modern challenger promising cheaper bills, smarter tariffs, and a consumer-first approach to power.

Millions of households bought into that vision. In fairness, Octopus achieved what few thought possible: within little more than a decade, it overtook legacy suppliers to become Britain’s largest household energy provider. But success can sometimes change a company’s purpose. Today, serious questions must be asked about whether Octopus is still fundamentally focused on serving the British consumer or whether its ambitions have outgrown the original mission that built its reputation.

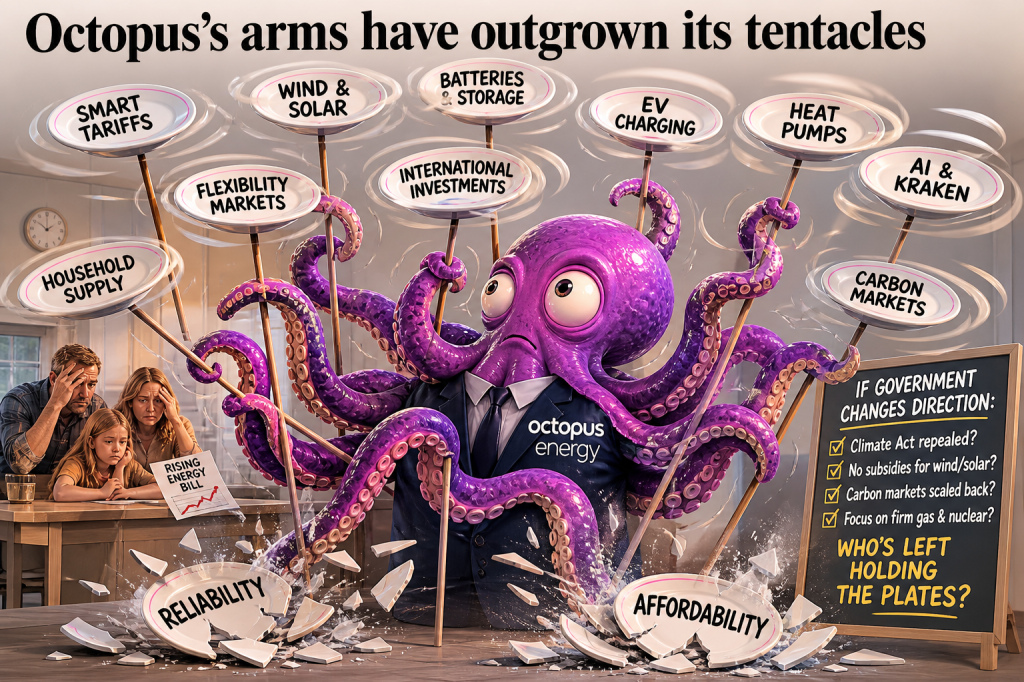

Octopus’s arms now stretch far beyond simply supplying electricity. The company is embedded in wind generation, solar investment, battery storage, electric vehicle charging, heat pumps, smart demand-response tariffs, AI-driven grid software through Kraken, and increasingly international infrastructure and carbon-linked investments. What once looked like a challenger energy supplier increasingly resembles a corporate ecosystem built around one political and economic model: Net Zero.¹

That is not, in itself, a crime. Businesses naturally adapt to political and market opportunities. But when a company’s growth becomes deeply intertwined with government policy, subsidy structures, climate mandates, renewable planning frameworks, and carbon-market economics, it also inherits political risk. And political winds, unlike climate targets, have a habit of changing direction.

Across Britain, serious political voices are now openly questioning the long-term affordability of the Net Zero model. Questions once dismissed as fringe , about grid instability, industrial competitiveness, farmland loss, subsidy dependence, carbon offsets, and rising household bills , are increasingly entering mainstream political debate. If a future United Kingdom government decides to review or fundamentally amend the Climate Change Act 2008, reduce subsidy-driven renewable expansion, or shift toward firm domestic generation through gas and nuclear, then companies built around the assumptions of the current energy transition may face a very different operating environment.²

That is where the old saying becomes relevant:

The higher you climb, the bigger the fall.

Octopus’s arms may now have outgrown its tentacles. The company that once promised to challenge the system now appears deeply embedded within it. And when executives begin discussing whether consumers might tolerate “the odd blackout” in return for lower prices, while simultaneously expanding into carbon markets, international offset schemes, AI platforms, and battery sales, the British public is entitled to ask a difficult question:

Has Octopus remained focused on serving households , or has it become too invested in monetising the Net Zero economy itself?

Consumers were promised cheaper energy. Instead, many face rising standing charges, rising network costs, more complex tariffs, and growing demands to alter their behaviour around when and how they use electricity. Meanwhile, the companies operating within this transition continue finding new commercial opportunities at every turn , whether in flexibility services, software, storage, or carbon accounting.³

If Britain changes course , as many believe it eventually will.Then some of the companies that climbed fastest under the old climate-policy model may face the hardest questions under the next one.

And perhaps that is the real issue.

If you helped shape the system and profit from the system, then you should be accountable for the consequences of the system , not asking the public to lower their expectations.

Shane Oxer. Campaigner for fairer and affordable energy

References

1. Octopus Energy corporate operations, generation portfolio, Kraken platform, retail expansion, and low-carbon services (public corporate disclosures).

2. Climate Change Act 2008 and subsequent UK Net Zero policy frameworks.

3. Ofgem price cap data, network charge increases, and standing charge methodology.

Leave a comment