Britain’s Net Zero Gamble Is Ignoring the Warnings Already Written Across Europe

By Shane Oxer. Campaigner for fairer and affordable energy

There comes a moment in every national policy when ideology collides with physics. Britain’s energy transition is rapidly approaching that moment.

For nearly two decades the British public has been told that if enough solar panels are installed, enough wind turbines approved, enough batteries announced, and enough gas plants retired, a cheaper, cleaner, and more secure electricity system will emerge almost automatically.

Yet when the rhetoric is stripped away and the engineering data examined, a more troubling picture appears:

Britain is moving towards the most ambitious energy transformation in its modern history while many of the foundations required to make it work remain unfinished.

Even more concerning is that the warning signs are no longer theoretical. They are already visible across Europe.

This week the Greek solar market delivered one of the clearest warnings yet. Greece, after years of aggressive renewable expansion, is now facing a growing crisis of curtailment, collapsing wholesale prices, and investor distress. Between January and April 2026 alone, Greek grid operators curtailed 876.5 GWh of renewable electricity , up sharply from 588.5 GWh during the same period a year earlier. Midday electricity prices, precisely when solar generation peaks, have repeatedly fallen to zero or below zero. Small and medium-sized solar producers have reportedly seen revenue losses of between 62% and 70% in just a matter of weeks.¹

The cause is not difficult to understand. Greece has installed approximately 17.9 GW of renewable capacity in a system where peak electricity demand is only around 11 GW. Solar electricity is flooding the grid when demand is weakest, yet when evening demand rises and solar disappears, gas and hydro remain the technologies that set prices. In other words, generation has been built faster than storage, demand growth, or grid flexibility can absorb it.

Britain may believe it is different.

But the laws of power systems do not change at Dover.

Our own grid data suggests Britain may be walking towards the same structural imbalance , only on a far larger scale.

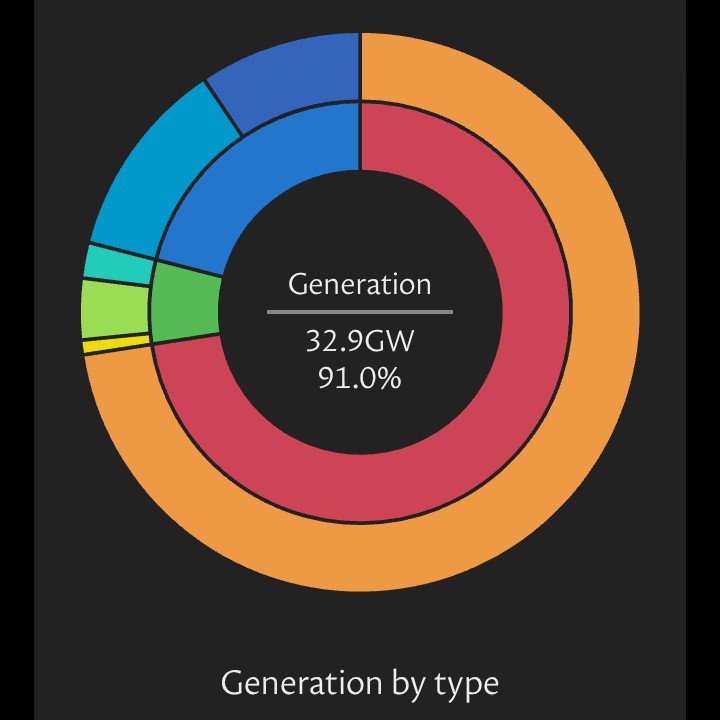

A detailed analysis of the UK Transmission Entry Capacity register shows a system now carrying 845 unique connection nodes, 1,554 live projects, and nearly 483,268 MW of queued generation and storage seeking access to the grid. Of that, more than 242,387 MW is solar-associated generation, while battery storage projects now account for over 470,691 MW of queued capacity.²

Those figures sound impressive , until one examines the delivery dates.

Across major substations from Yorkshire to Lincolnshire, Derbyshire to East Anglia, effective grid connection dates repeatedly stretch into the 2030s, with some projects not due until 2037–2039. Key sites including Thorpe Marsh 400kV Substation, Brinsworth 400kV Substation, and Creyke Beck 400kV Substation all show connection constraints extending years beyond current political promises.²

This matters because politicians often talk in installed capacity, while engineers work in delivered power.

Planning approval is not generation. A press release is not electricity. A ministerial target is not grid stability.

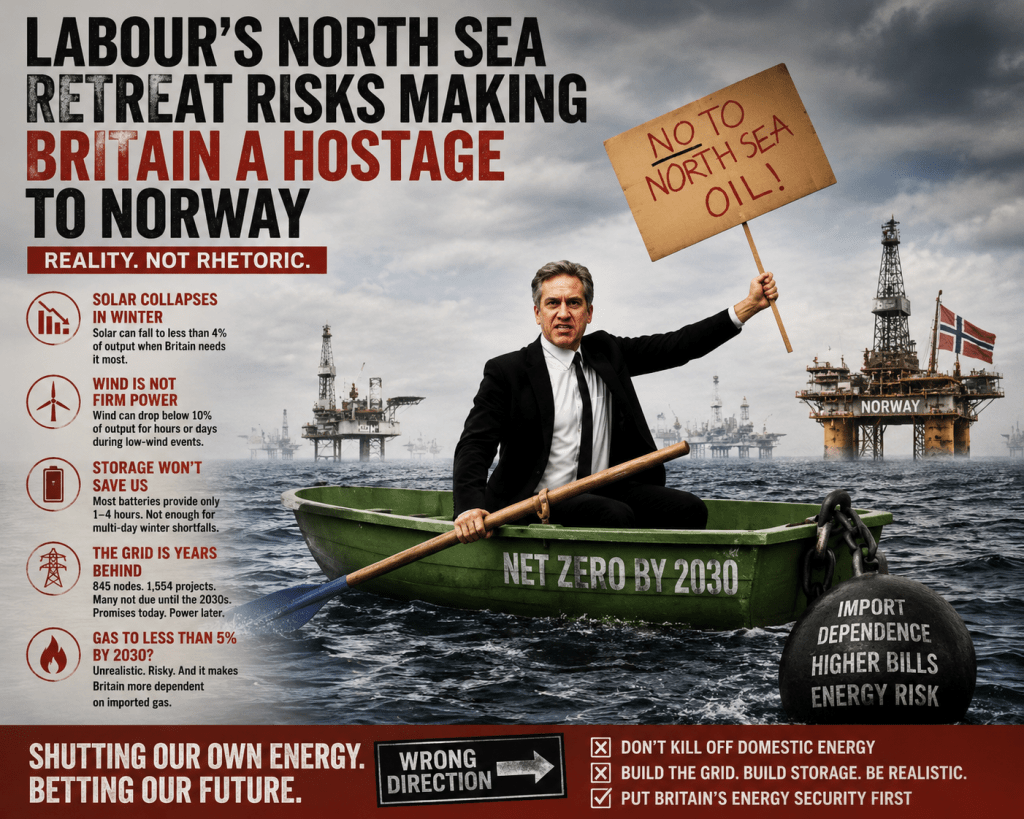

The government’s own Clean Power 2030 pathway expects gas-fired generation to fall to below 5% of electricity generation by 2030. Yet Britain has already closed coal generation, existing nuclear stations are ageing, and major replacements such as Hinkley Point C and Sizewell C are unlikely to provide substantial relief until the early-to-mid 2030s.³

That leaves one unavoidable question:

What exactly fills the gap?

Solar certainly does not.

In Britain, solar generation performs worst when demand is highest. Winter brings short days, weak sun angles, persistent cloud cover, and peak electricity demand that often occurs after sunset. No amount of political spin can change the fact that solar output collapses precisely when households need heat, light, and resilience the most.

Wind is often presented as the answer. Yet wind, while valuable across a year, is not firm power. During prolonged high-pressure systems , particularly cold winter anticyclones , wind output can fall sharply across large parts of the British Isles. At those moments, the system falls back on gas, imports, hydro, and what remains of Britain’s dispatchable generation fleet.

Battery storage is often promoted as the final piece of the puzzle. Yet most battery systems currently being deployed across Britain are designed for one to four hours of discharge, not for the multi-day low-wind events that routinely threaten winter system stability. Batteries can balance short-term volatility. They cannot yet replace several days of missing generation at national scale.⁴

Which brings us to the uncomfortable truth.

Britain appears to be pursuing the largest transformation of its electricity system in generations while removing reliable generation faster than replacement infrastructure is physically being delivered.

At the same time, domestic gas production is being suppressed, making Britain increasingly reliant on imported fuel from countries such as Norway and LNG markets increasingly influenced by global events. Energy sovereignty is quietly being exchanged for infrastructure promises that, according to the grid data itself, may not fully materialise until the late 2030s.

Europe is already showing what happens when ideology outpaces engineering.

Germany has experienced growing curtailment and market cannibalisation.

Spain has battled oversupply pricing pressures.

Greece is now watching small renewable investors pushed towards financial collapse.

And Britain?

Britain is still telling the public that everything will be ready by 2030.

The evidence increasingly suggests otherwise.

If ministers fail to confront the physical limits of solar, the intermittency of wind, the reality of storage constraints, and the growing backlog in Britain’s grid infrastructure, then the result will not simply be higher bills.

It will be a national energy reckoning.

And when that reckoning arrives, it will not be caused by a lack of ambition.

It will be caused by ignoring the warnings that were already visible elsewhere.

References

1. pv magazine� — “Curtailment, negative prices push Greek small- and medium-sized PV asset owners toward bankruptcy,” 7 May 2026.

2. UK TEC Substation Node List – Solar / Wind Split (user-supplied grid analysis), April 2026. �

UK_TEC_full_table.docx

3. EDF Energy� project updates and UK nuclear delivery schedules.

4. National Energy System Operator battery balancing and grid flexibility modelling.

Leave a comment